What Kalpana’s quiet habit reveals about money behaviour

Raju’s house had the kind of calm you only notice when it’s missing, pressure cooker whistles in the morning, chai on the stove, a calendar near the fridge stuck on last month, and a kitchen that always smelled like jeera tadka. It was a regular, middle-class Indian home where life moved on routine and trust.

Raju, in his mid-fifties, ran a small business; steady, relationship-driven, built slowly over years. Kalpana was a homemaker, the kind who kept the family running without anyone noticing how much thinking it took. Their sons, Dhyey and Dharam, were well-mannered, sincere at studies, and the kind of boys elders liked instantly. Dhyey was older by two years, naturally the “I’ll handle it” one. Dharam was quieter, observant, the one who understood mood before words.

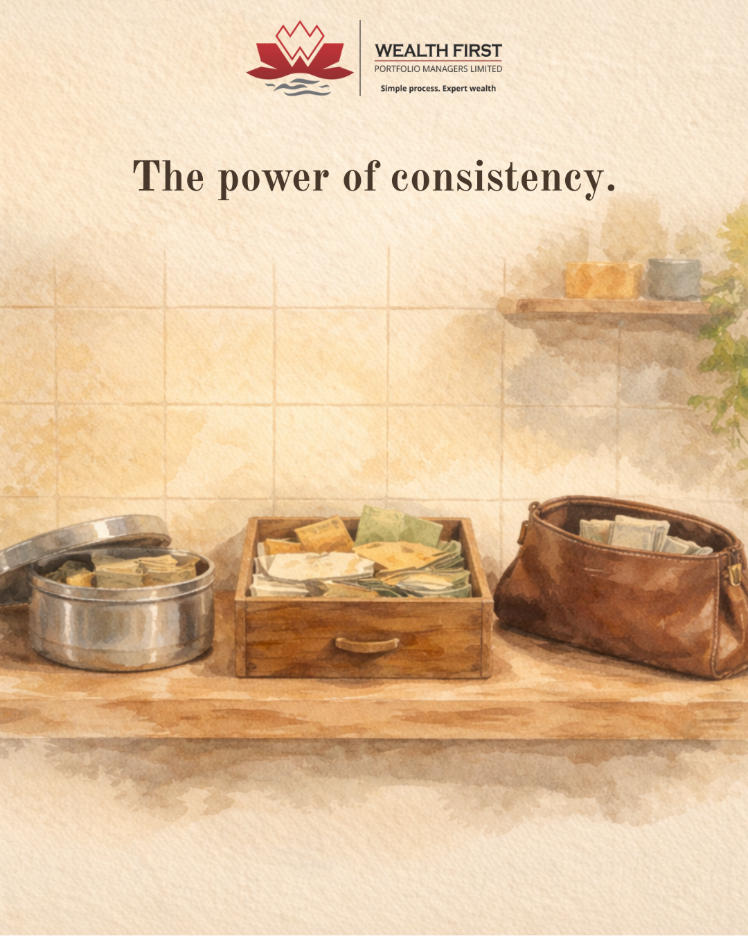

Kalpana had one habit no one knew about. Not because it was dramatic, but because it was so normal it blended into her day. Every month, after expenses were managed, she would quietly keep away a little money. Sometimes ₹200, sometimes ₹500, sometimes just a folded note saved from careful spending. She didn’t call it saving. She didn’t announce it. She simply placed it, faithfully, into three different spots: a small dabba in the kitchen for her own savings, a cupboard drawer for the children and extra expenses, and an old unused purse for emergencies. Three places. Three purposes. No speeches.

Life was smooth until one evening, it wasn’t.

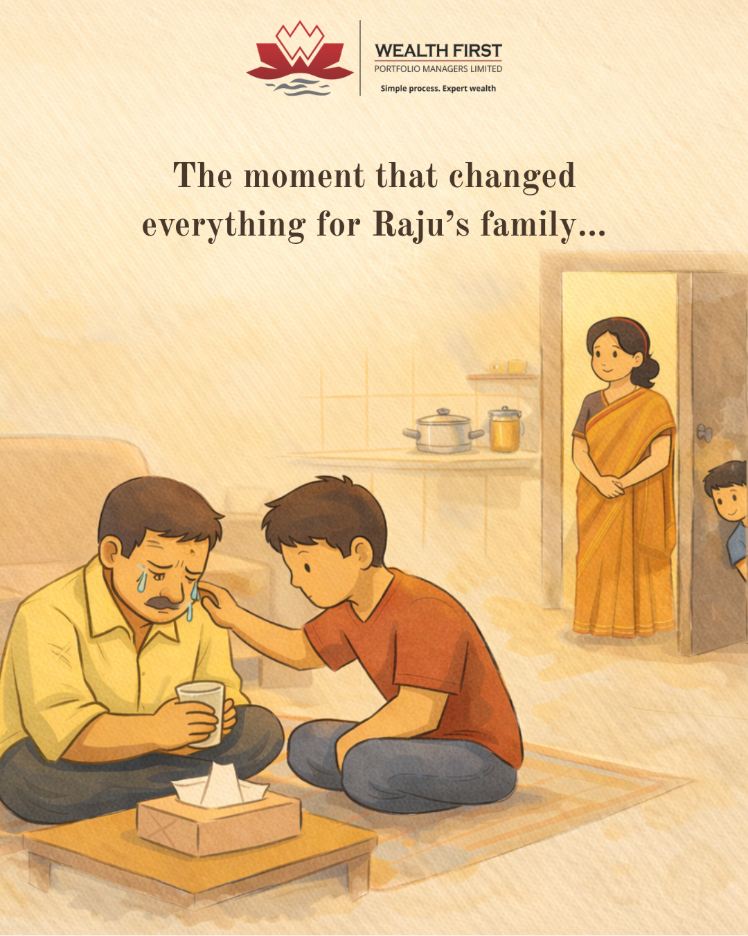

Raju came home early, but not in a relaxed way. His slippers dragged. His face looked like it had been carrying weight for hours. He sat down without asking for water, staring at the floor like the answer might be hiding there. Dhyey noticed instantly and sat beside him, quiet first because some storms need silence before solutions.

Raju finally spoke, voice low. “Someone… fooled me.”

A buyer had taken goods and promised payment, then disappeared. No response, no proper trail, nothing that could bring money back quickly. For a small businessman, the loss wasn’t only financial, it was personal. It was shock, shame, and fear trying to look like control.

Dhyey asked the practical question. “Papa… loan?”

Raju’s reply came too quickly, like pride was trying to protect him from panic. “Never. I’ve never taken a loan in my life.” The sentence sounded firm, but his eyes didn’t.

Dharam stood near the doorway, listening. Dhyey stayed quiet, because he could see his father wasn’t refusing a loan; he was refusing the feeling of helplessness. Raju rubbed his forehead. “Maybe I should sell some gold,” he said, testing the words like they tasted bitter.

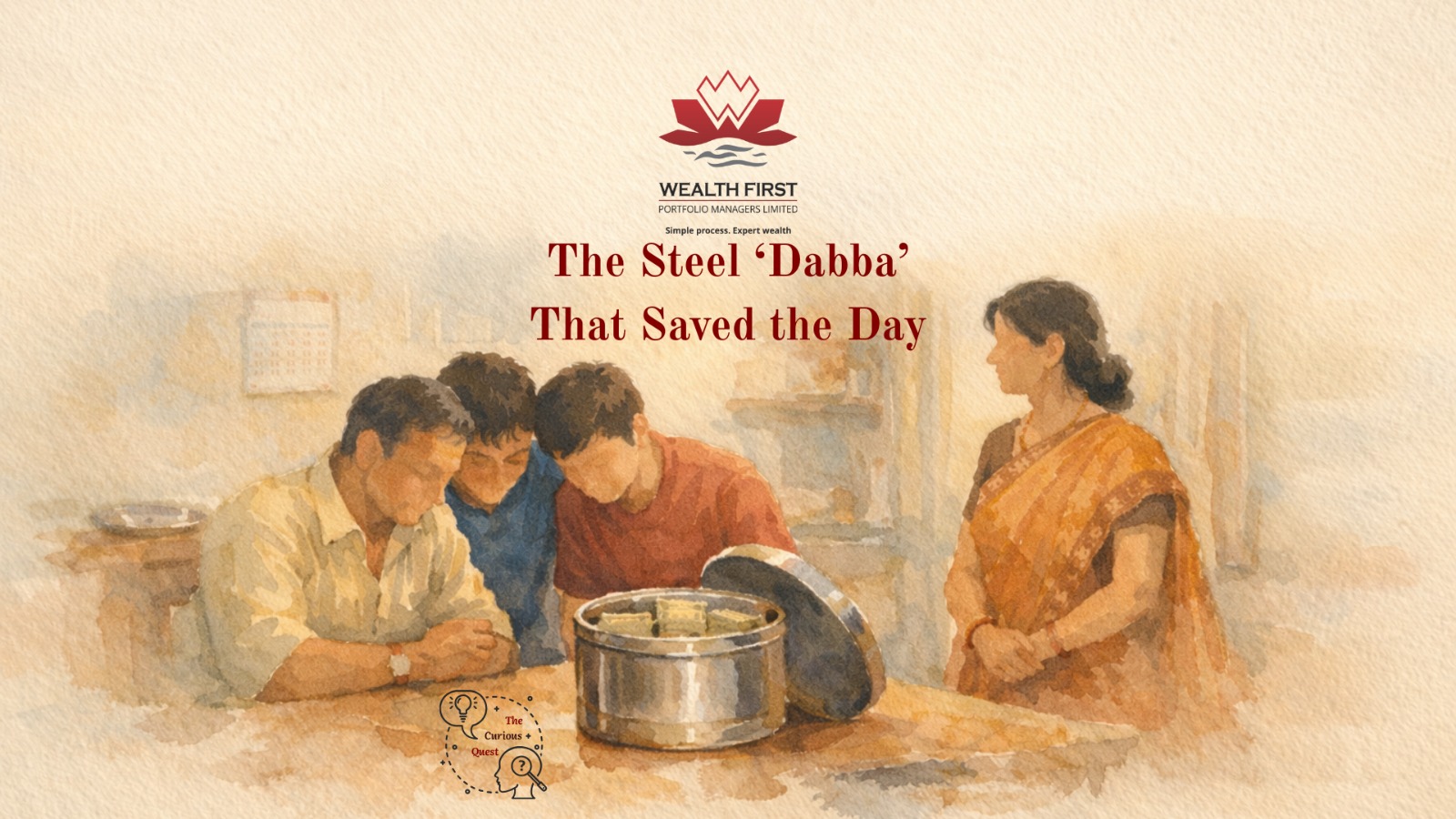

That’s when Kalpana walked in.

No dramatic gasp. No “what happened” hysteria. She came in with the calm of someone who had been preparing for life’s surprises without naming them. In her hands was a large steel dabba. She placed it on the table in front of Raju and Dhyey.

Raju looked up, confused. “What is this?”

Kalpana didn’t say anything. She just gave a calming and reassuring look and smiled at him. She just uttered, “Look for yourself.” Raju quickly went near the dabba and lifted the lid and froze.

The dabba was filled with money. Neatly folded notes, layered like months of patience. Dhyey’s eyes widened. Dharam stepped closer. The room, which had been heavy a moment ago, suddenly felt like it had more oxygen.

Kalpana said softly, “This is from my savings. And the emergency purse. I kept it… for a day like this.”

They counted it. It wasn’t some magical jackpot. It was simply the power of consistency. And it was almost enough to cover the loss. A small amount still remained, but the conversation had already changed. Raju’s shoulders dropped, not with defeat, but with relief. The helplessness loosened its grip. He looked at Kalpana, voice breaking in a place pride couldn’t reach. “Why didn’t you tell me?”

Kalpana gave a small, practical smile. “Because you would’ve said, ‘Arre, itna kyun sochti ho?’” She paused, then added, “And because I wasn’t saving for a festival. I was saving for peace.”

That night, Raju still couldn’t sleep early. But it wasn’t panics keeping him awake now. It was planning how to recover the small remaining amount, how to tighten controls, and how to rebuild. The dabba hadn’t only saved money. It had saved the most important thing in that room: the courage to face tomorrow.

The Money Behaviour This Reveals

Kalpana unknowingly did something financially mature: she separated money by purpose; personal buffer, children/irregular expenses, and emergencies. That’s real diversification: not just different “investments”, but different buckets for different shocks. The next step is to make this system safer, trackable, and less dependent on one person’s memory.

Calm Rule

Don’t keep your entire safety net in one place. Create separate buckets for (1) monthly life, (2) known surprises, and (3) real emergencies.

The 15-Minute Habit

This weekend, create three labelled money buckets (bank accounts, envelopes, or digital jars):

- Everyday (monthly buffer)

- Irregular (fees, repairs, festivals, OPD, gadgets, travel)

- Emergency (job/business loss, hospitalisation)

Then set one tiny routine: auto-transfer even ₹500–₹1,000 monthly into the Emergency bucket. Consistency beats intensity.

Review Cadence

Monthly (same date as income): top-up Emergency, refill Irregular if used, and keep only practical cash at home.

Half-yearly: raise your emergency target as expenses rise, and shift “secret stashes” into safer, trackable options.

Quest Question

If an unexpected loss hits your home next month, which bucket will protect your peace first and is it big enough today?