Insurance usually enters our conversations after something goes wrong; an accident, a hospital bill, or a sudden loss in the family. But the purpose of insurance is to ensure that a tough moment does not become a long-term financial setback.

In India, this matters deeply because responsibilities are often shared across generations. When one income supports many, uncertainty is not just personal; it is family wide. This guide explains insurance in simple terms: what it is, how it works, major types, key benefits, and the practical mistakes to avoid.

What Is Insurance?

Insurance is a financial arrangement designed to protect you from large, unexpected losses. You pay a premium, and in exchange, the insurer agrees to pay for certain losses or provide benefits as defined by the policy terms.

Think of it as financial continuity. You are not buying fear; you are building a buffer so that life does not force you into rushed decisions like breaking long-term savings, selling assets in distress, or borrowing at high interest.

How Does Insurance Work?

At a practical level, insurance works through risk pooling:

1) You Pay a Premium

A premium is the amount you pay at agreed intervals to keep the policy active.

2) The Policy Defines What’s Covered

Coverage includes what the insurer will pay for, under what conditions, and up to what limit.

3) You Raise a Claim When a Covered Event Happens

When a defined event occurs, you intimate the claim and submit documents. The insurer assesses it and pays as per the policy.

Key Terms You Should Understand

- Coverage / Sum insured / Sum assured: the protection amount (structure differs by product type).

- Policy limit: maximum amount payable.

- Deductible (common in health/general insurance): amount you pay before insurance starts paying.

- Exclusions: what is not covered.

- Waiting period (often in health): coverage may begin after a defined time for specific conditions.

- Co-pay / sub-limits (health): shared cost or caps that affect out-of-pocket expenses.

Most dissatisfaction happens when people assume insurance is “everything covered”. It is not. It is contract-based protection.

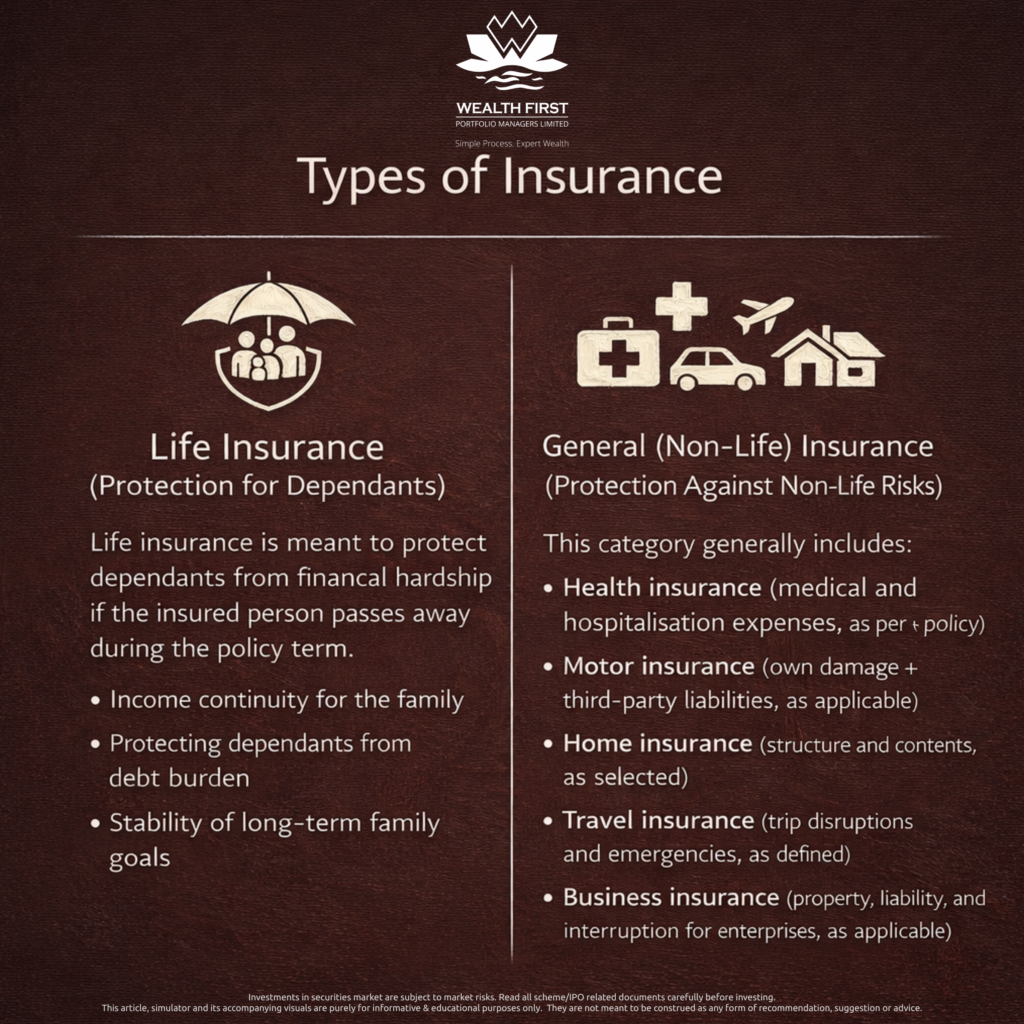

Types of Insurance

Insurance is commonly grouped into life and general (non-life) insurance. The goal here is clarity not product recommendations.

1) Life Insurance (Protection for Dependants)

Life insurance is typically meant to protect dependants from financial hardship if the insured person passes away during the policy term.

What it tries to solve:

- income continuity for the family

- protecting dependants from debt burden

- stability of long-term family goals

2) General (Non-Life) Insurance (Protection Against Non-Life Risks)

This bucket generally includes:

- Health insurance (medical and hospitalisation expenses, as per policy)

- Motor insurance (own damage + third-party liabilities, as applicable)

- Home insurance (structure/contents, as selected)

- Travel insurance (trip disruptions/emergencies, as defined)

- Business insurance (property/liability/interruption for enterprises, as applicable)

Many households face “financial leakage” not because they did not earn enough, but because a single unplanned expense forced them to liquidate savings at the wrong time.

Why Insurance Is Important (Especially in India)

Insurance matters because it protects more than money it protects stability.

1) It Prevents Goal Derailment

Without protection, emergencies can consume funds meant for education, home goals, or retirement.

2) It Reduces Distress Decisions

Selling long-term assets quickly or borrowing at steep rates often causes second-order damage.

3) It Protects Family Dignity and Peace of Mind

When support systems are already stretched, insurance reduces the financial panic that follows a crisis.

Key Benefits of Having Insurance

Here are the benefits in real-world terms:

- Financial shock absorption: handles large expenses that are hard to manage from monthly cashflow

- Stability for dependants: reduces sudden income-gap stress (where relevant)

- Asset protection: reduces the need to sell investments or gold during emergencies

- Liability protection: in certain cases, protects you from third-party financial liabilities (policy-dependent)

- Better planning confidence: helps households plan knowing risks are partially ring-fenced

Important note: Benefits depend entirely on policy terms, limits, and exclusions.

Common Mistakes Indians Make with Insurance (And How to Avoid Them)

1) Buying in a Hurry

Insurance bought in panic often leads to poor fit and later disappointment. Always read exclusions and key limits calmly.

2) Underinsuring to Reduce Premium

A low premium can feel good monthly but may be inadequate during a real event. Aim for meaningful protection, not token cover.

3) Incomplete or Incorrect Disclosures

Misrepresentation can create claim complications. Accurate information protects you later.

4) Letting Policies Lapse

A lapsed policy is effectively no protection. Set reminders and keep records.

5) Not Updating Nominee/Beneficiary Details

Life changes (marriage, children, loss in family) should trigger updates.

A Simple Checklist Before You Buy Any Insurance

This is a neutral checklist readers can use without any product push:

- What risk am I protecting against health costs, accident liability, income loss, property damage?

- What are the top exclusions and waiting periods?

- What are the limits, deductibles/co-pay clauses, and sub-limits (if applicable)?

- What documents are required for claim intimation?

- Where is the policy stored, and who in the family knows how to access it?

- Are nominee/beneficiary details current?

Insurance as a Quiet Form of Care

Insurance is not about pessimism. It is a practical form of care because it acknowledges that uncertainty is part of life. For Indian families, the real value is not only the claim payout, but the ability to protect the future plans you have built patiently.

References:

Department of Financial Services, Ministry of Finance, Government of India. “Insurance Overview.”

Insurance Regulatory and Development Authority of India. Insurance Advertisements and Disclosure Regulations, 2021.

Kagan, Julia. “What Is Insurance?” Investopedia.

MetLife. “What Is Insurance: Definition & How It Works.”

Press Information Bureau, Government of India. “Plying Motor Vehicles without Valid Motor Third Party Insurance is a Punishable Offence.”