Wealth First Explains the regulatory framework behind India’s alternative investment vehicles

After knowing about ‘what is an AIF?’ in Part 1, Part 2 is a deep dive into it. As indicated in the first part, AIFs are not one product. They’re a regulated framework of strategies.

SEBI has done something very deliberate in the AIF regulations: it has grouped AIFs into Category I, II, and III, based on what they invest in and how they operate (especially around complexity and leverage/borrowing).

Think of it like this:

- some funds are designed to build (early-stage, infrastructure, socially meaningful),

- some are designed to participate (private equity, debt, without leverage),

- and some are designed to trade/hedge more actively (complex strategies, possible leverage).

That’s the core logic of categorisation. A quick way to read an AIF is: category first, strategy next, governance always.

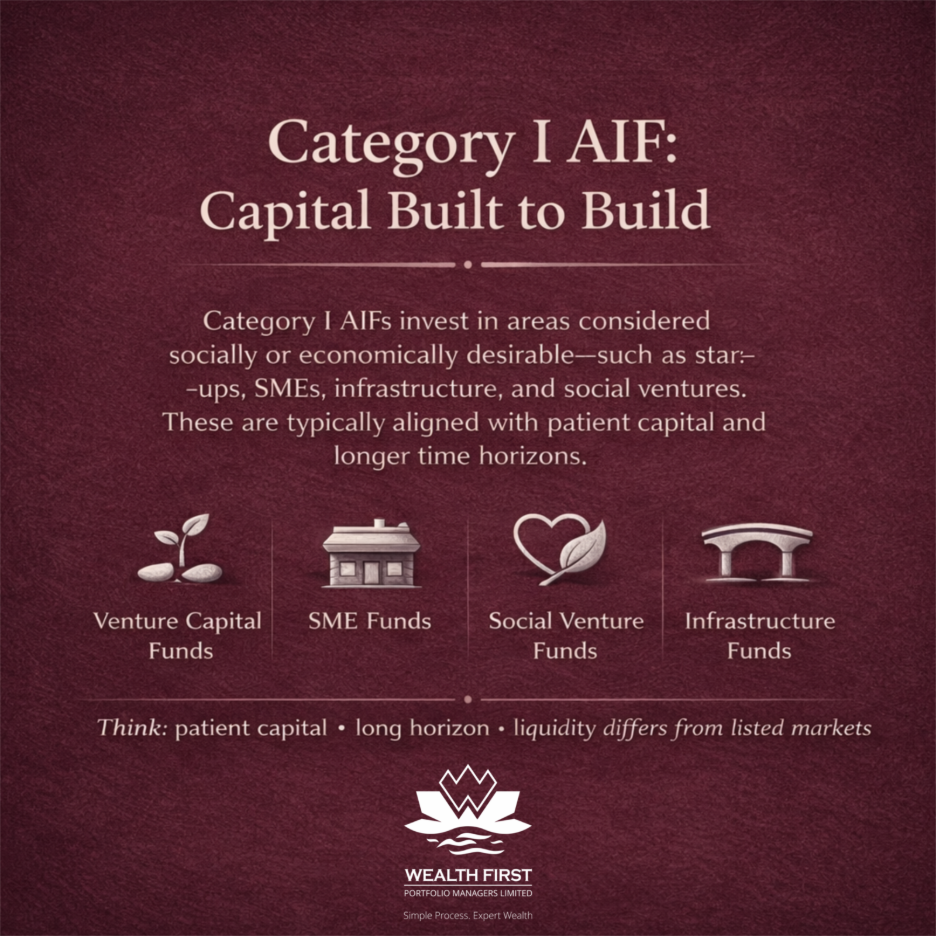

Category I AIF: capital that is meant to “build”

Category I Alternative Investment Funds (AIFs) are SEBI-regulated funds that primarily invest in socially or economically beneficial sectors such as infrastructure, startups, small and medium enterprises (SMEs), and social ventures.

In summary, Category I generally aligns with “patient capital” that supports building enterprises or infrastructure or meeting social goals where outcomes are often long-term, and liquidity is not the same as listed markets.

Category II AIF: private equity / private credit style, without leverage (as a rule)

Category II is defined as AIFs that do not fall under Category I or III and do not undertake leverage or borrowing other than as permitted in the regulations. SEBI’s explanation also indicates that Category II typically includes funds like private equity or debt funds where no specific incentives or concessions are provided by the government or other regulators.

In plain terms, if Category I is “build”, Category II is often “own or lend privately” with a structure that isn’t primarily about complex trading.

Category III AIF: complex strategies, including hedge fund styles

Category III is where SEBI has placed funds that employ diverse or complex trading strategies, and may use leverage, including through investment in listed or unlisted derivatives.

SEBI’s explanation also frames hedge funds as AIFs that trade with an aim to make short-term returns or pursue other open-ended strategies and includes such funds within Category III.

Why SEBI separates Category III

Because once strategies become more complex and can involve leverage and derivatives, the risk and monitoring expectations change. Categorisation helps create a clearer regulatory lane.

A closer look at some important defined AIF “types”

The regulations define multiple fund types that commonly show up in AIF conversations. A few are particularly relevant for understanding the ecosystem:

1) Venture Capital Fund (VCF) & Venture Capital Undertaking

A venture capital fund is described as an AIF investing primarily in unlisted securities of start-ups / emerging / early-stage venture capital undertakings, often tied to new products, services, technology, or intellectual property-based activity.

2) Infrastructure Fund

Defined as an AIF investing primarily in entities/SPVs engaged in infrastructure projects, aligned to the scheme’s mandate.

3) Private Equity Fund

An AIF investing primarily in equity/equity-linked instruments or partnership interests of investee companies, as per the stated objectives.

4) Hedge Fund

An AIF employing diverse/complex trading strategies and investing/trading in securities involving diverse risks or complex products (including listed/unlisted derivatives).

5) Social Impact Fund and Social Venture

The regulations define “social impact fund” and “social venture” concepts, along with “social units” as provided for under the framework (issued for social impact funds/schemes to investors who agree to receive only social returns/benefits rather than financial returns). This is a distinct part of the AIF ecosystem, meant to structurally recognise “impact-first” participation.

Now, for the part that quietly defines who AIFs are built for: the entry gates.

Investor thresholds for AIFs

SEBI’s regulations build in minimum size thresholds at two levels: scheme size and investor contribution, reflecting that AIFs are meant for sophisticated participation.

Minimum scheme corpus

- Each scheme of an AIF must have a corpus of at least ₹20 crore.

- For social impact fund schemes, the minimum corpus is ₹5 crore.

Minimum investment per investor

- An AIF generally shall not accept an investment from an investor below ₹1 crore.

- For employees/directors of the AIF / Manager / Sponsor, the minimum may be ₹25 lakh (as per the regulation’s stated exception).

- For accredited investors, however, the minimum investment condition is set differently (more on this later).

- For a social impact fund investing only in securities of not-for-profit organisations registered on a social stock exchange, the minimum investment by an individual investor can be ₹2 lakh (as per the stated provision).

These thresholds are one reason AIF participation is generally positioned for higher-ticket, sophisticated investors under the framework.

Accredited Investor and the “Large Value Fund” construct

The regulations define “accredited investor” with eligibility criteria (covering individuals, HUFs, family trusts, body corporates, partnership firms) based on income / net worth / financial asset thresholds and requiring accreditation by an accredited agency.

They also define a “large value fund for accredited investors” an AIF/scheme. As of late 2025, SEBI has reduced this threshold to deepen participation in these sophisticated vehicles. SEBI has updated certain relaxations for LVFs for accredited investors (refer to latest SEBI amendments/circulars for the prevailing threshold).

In simple terms: SEBI recognises that extremely large-ticket, highly sophisticated participation can sit in a distinct bucket.

Registration and eligibility: the “guardrail architecture”

SEBI requires that entities acting as AIFs obtain registration, and it lays down an eligibility lens for considering an applicant. It evaluates applications against eligibility conditions specified under the framework.

Some key aspects in plain language:

- The fund must be properly formed (company / trust / LLP structure documents).

- The fund’s documentation should not allow a public invitation to subscribe.

- Sponsor/Manager must be fit and proper.

- The investment team must have relevant experience/qualification as specified (the regulation lists experience/qualification expectations and allows SEBI to specify/recognise certifications).

- The applicant should have necessary infrastructure and manpower.

- At registration stage, the fund should clearly describe its objective, target investors, corpus, strategy/style, etc.

Also, an operational nuance that matters: SEBI provides that where an AIF has in-principle approval, it may accept commitments, but it shall not accept monies until the registration is granted.

Strategy changes can’t be casual

SEBI expects AIFs to state their strategy in documentation, and requires investor consent for material changes specifically, at least two-thirds of unit holders by value. This is an important “respect the mandate” principle.

Units and form

The regulations provide that AIFs issue units, and that the AIF shall issue its units in dematerialised form subject to conditions specified by SEBI.

AIFs exist because capital, like people, has different purposes. Some capital wants to help a business become real. Some want structured participation in private markets. Some want to express a view through complex strategies. Some want impact first.

SEBI’s AIF framework doesn’t tell anyone what to choose. It does something more important: it sets out the rules of the road; who can run such funds, how they must be structured, how strategies are disclosed, and how investor interests are protected through defined thresholds and consent requirements.

Key Takeaways

- Start with the category: Category I / II / III isn’t a label; it signals how the fund is built (patient capital), structured to own/lend (typically without leverage), or designed for complex trading/hedging (may use leverage).

- Read the strategy like a blueprint: The placement memorandum is the fund’s “operating manual” – objective, investible universe, limits, decision process, and what changes require investor approval.

- Know the entry gate: Check minimum investment, scheme corpus, and whether accredited investor conditions change applicability. (AIF participation is intentionally designed for sophisticated investors.)

- Check who is accountable: Look at the Manager/Sponsor, governance roles, and whether the framework requires “fit and proper”, capability, and operational readiness.

- Ask: what happens if the plan changes? Material strategy changes are not meant to be casual;consent thresholds exist to protect the mandate.